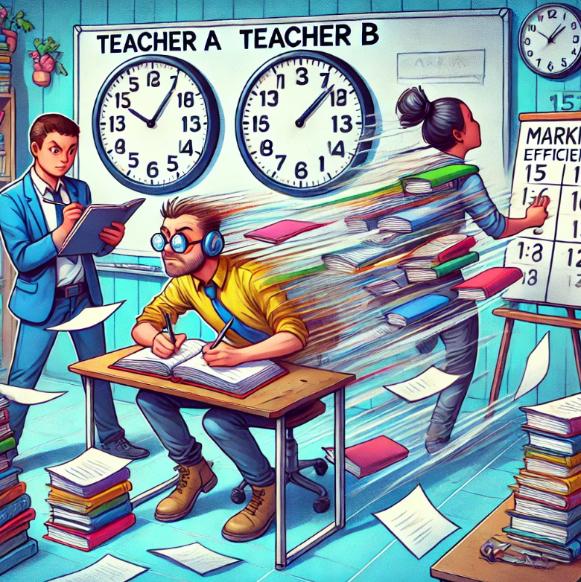

Question 1: Which teacher is the most efficient?

Teacher B @16 books per hour!

Question 2: Do you give anybody a pay rise?

The question is asking for other factors to be considered!

Teacher B is the most efficient, but what is the overall standard? Is it just tick and flick or is there serious marking going on?

What were the results last year in terms of books per hour marked?

How does these results compare to other departments?

Other factors are worth considering – beyond just the number presented.

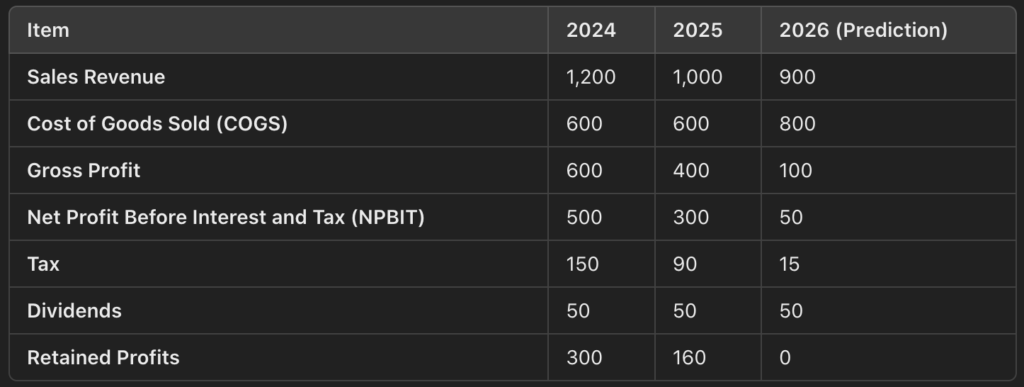

Question 3: Using the formula, calculate the gross profit margin for 20024, 2025 and 2026

2024: $1,20000 – $600,000 = $600,000 (2024: 600,000 / 1,200,000 * 100 = 50% )

2025: $1,000,000 – $600,000 = $400,000 (2025: 400,000 / 1,000,000 * 100 = 40%)

2026 (predicted): $900,000 – $800,000 = $100,000 (2026 (predicted): 100,000 / 900,000 * 100 = 11.1%)

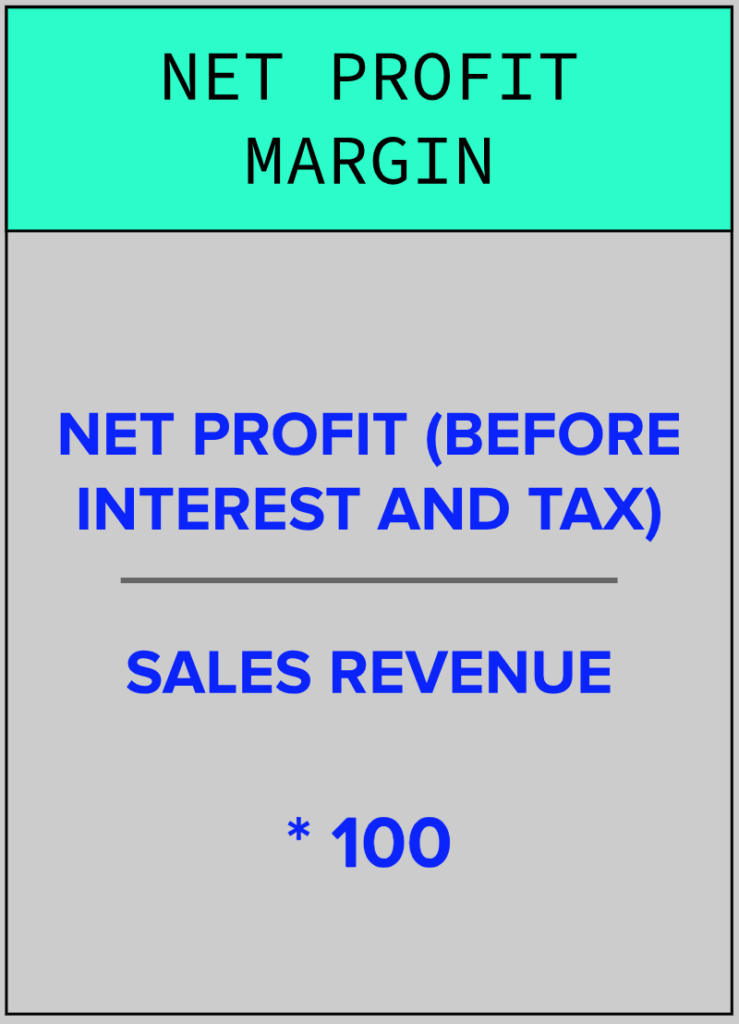

Question 4: Using the formula, calculate the net profit margin for 20024, 2025 and 2026

2024: 500,000 / 1,200,000 * 100 = 41.6%

2025: 300,000 / 1,000,000 * 100 = 30%

2026 (predicted): 50,000 / 900,000 * 100 = 5.5%

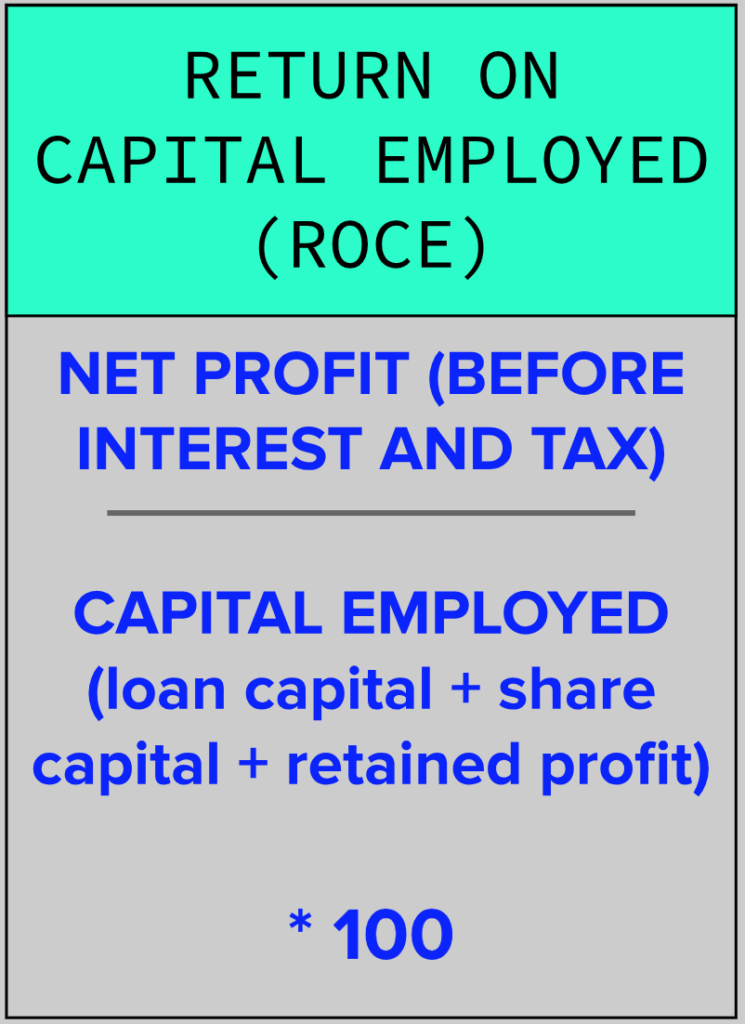

Question 5: Using the formula and information from BOTH the P&L and Balance Sheet, calculate the Return on Capital invested (ROCE)

ROCE = Net profit (before interest and tax) / Loan capital + Ordinary Share capital + Retained profits

300 / (100 + 160 + 400) * 100 = 45.45%

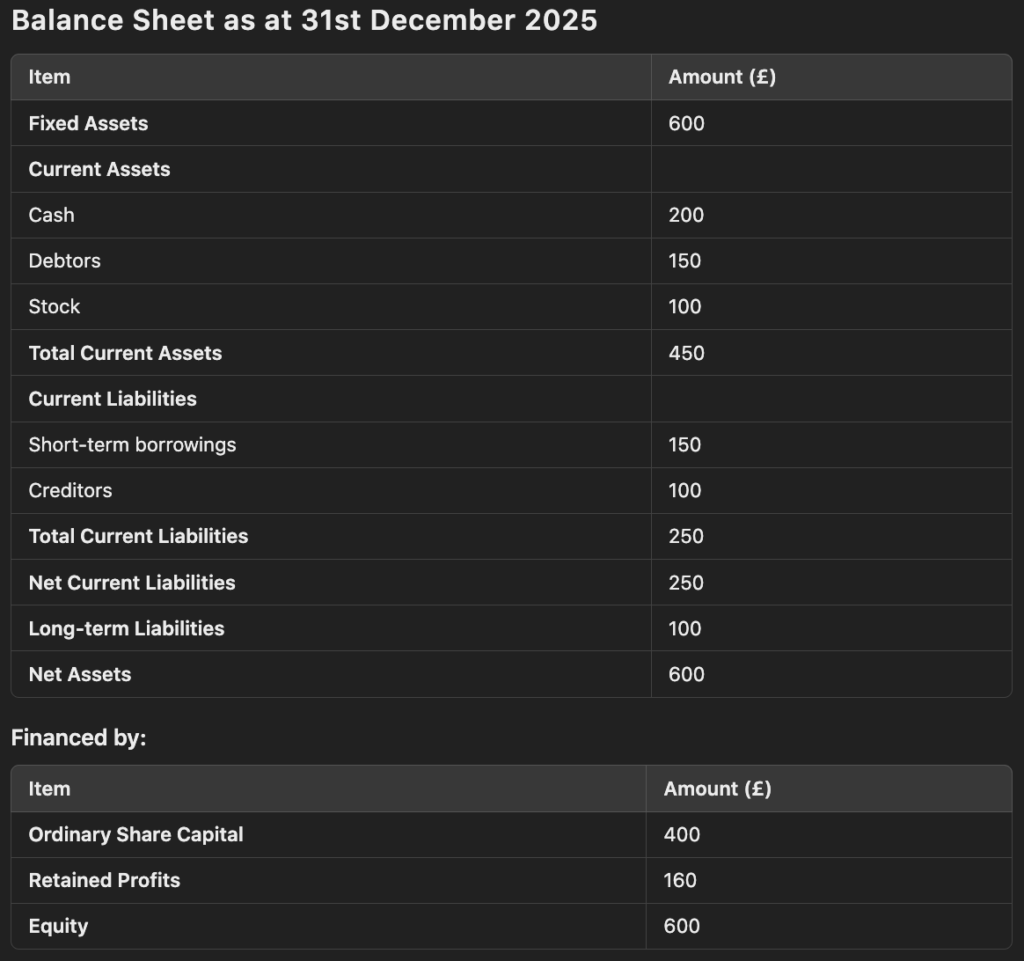

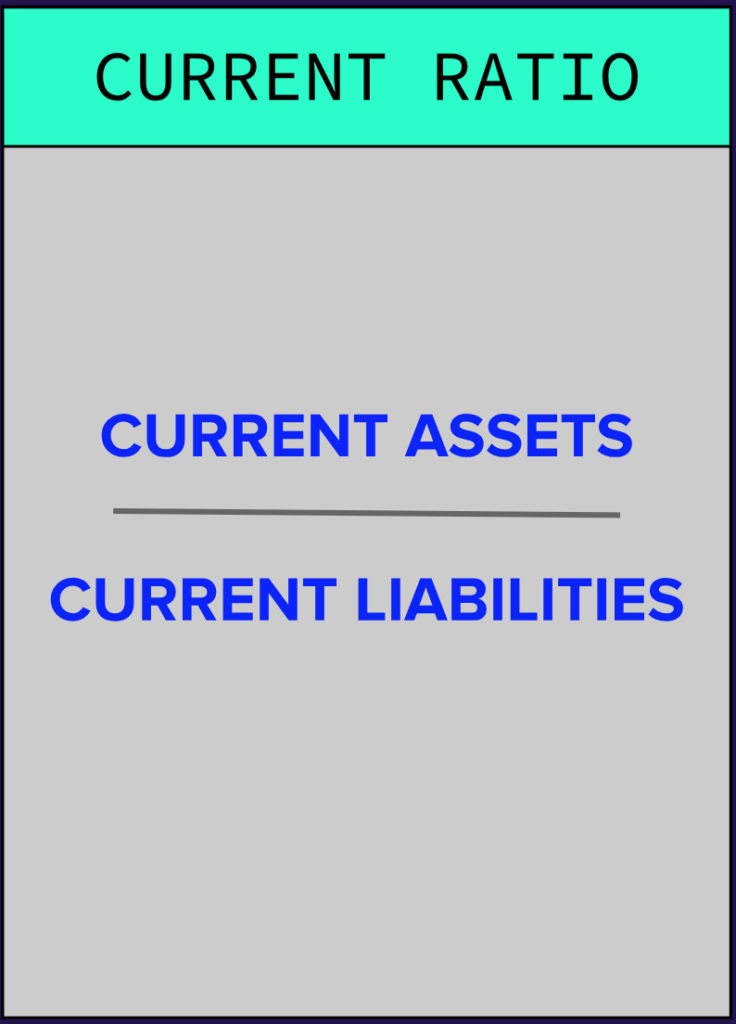

Question 6: Using the data given, calculate the current ratio for the business

Current assets / current liabilities: 450 / 250 * 100 = 1.8 : 1

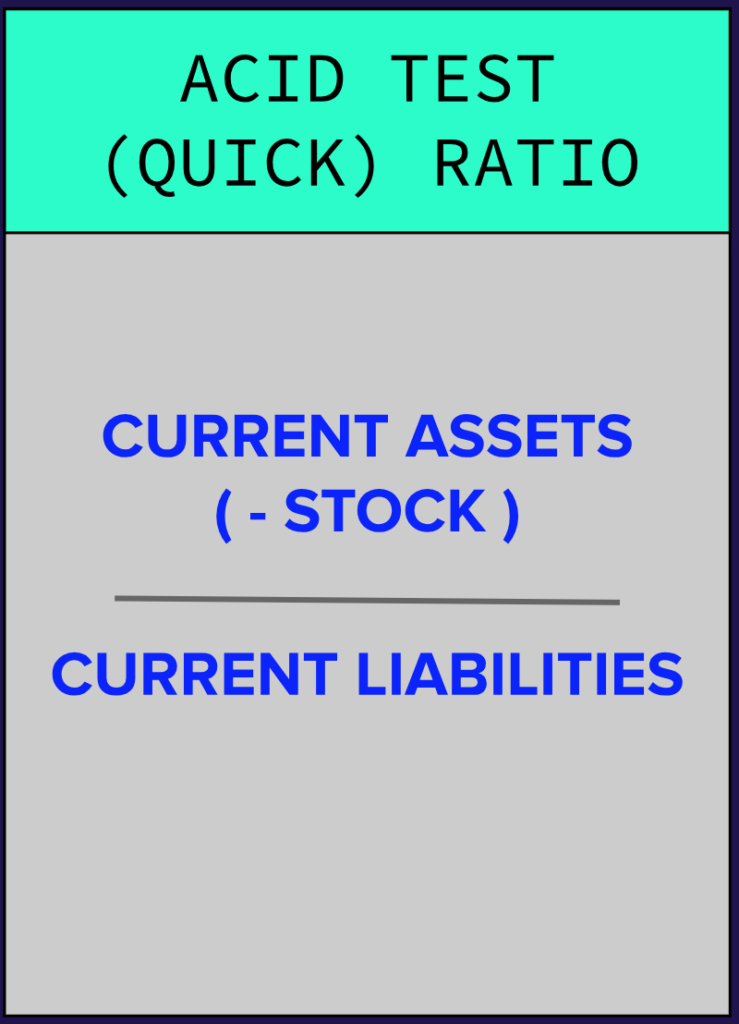

Question 7: Using the data given, calculate the acid test ratio for the business

Current assets (stock) / current liabilities : 350 / 250 * 100 = 1.4 : 1

Question 8:

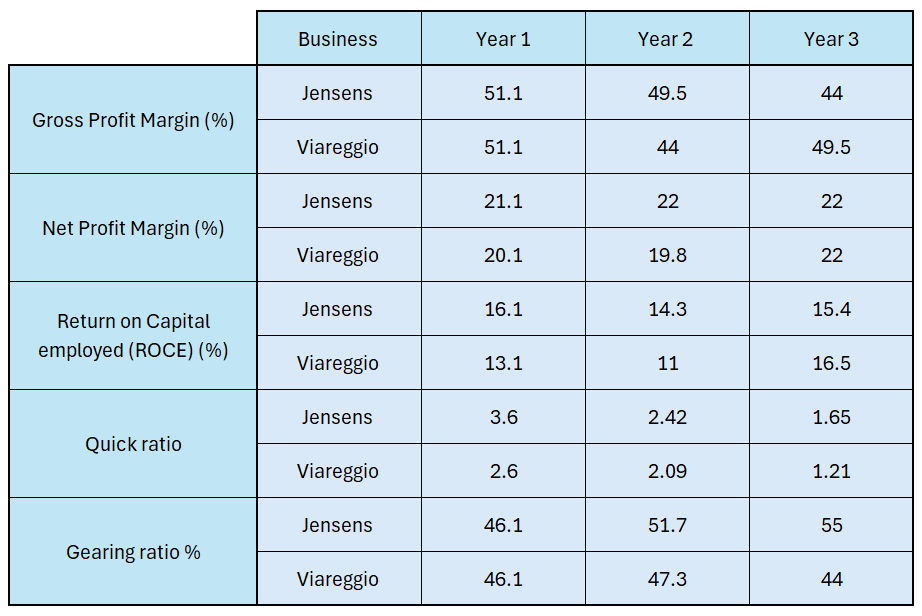

a) Discuss the relative attractiveness of Jensen’s versus Viareggio to potential examining the ratios [6]

Gross profit for both businesses has declined across the 3 year period.

Meanwhile – net profit has increased. This indicates a problem with COGS and the cost of goods sold! Viareggio has outperformed Jensen’s in this ratio – which indicates the cost control (cost of goods sold) has been better!

Both businesses improved their net profit though Viareggio by a greater (though negligible margin)!

The ROCE ratio has fallen for Jensen’s whereas Viareggio has seen a 3.4% increase! Over a 3 year period, neither ROCE value is good enough to compensate investors for the risk taken, but Viareggio has still outperformed Jensen’s. A ROCE value should equal (at the absolute minimum) the market rate of interest plus a risk factor payment. The ROCE values should be compared to a market average or industry average to show to what extent they underperformed!

In terms of quick ratio, both companies had slightly excessive levels of current assets (both over 2 : 1) which shows a degree of inefficiency. These excess current assets could have been better utilised elsewhere! Perhaps this could be linked to poor ROCE values!

However, by the end of the 3 year period, both businesses have reduced their ratio to acceptable levels (closer to 1 : 1).

Gearing ratio indicates that Jensen’s has the higher gearing, which suggests it carries a higher risk of default, higher debt repayment. Given the higher risk, the ROCE is worse because investors will be expecting to be compensated for taking a higher risk that comes with higher gearing,

b) Question 9: Discuss how these ratios could be improved [6]

Stock Turnover Days

- Reduce inventory levels: Implement just-in-time (JIT) stock management to avoid overstocking.

- Increase sales: Enhance marketing efforts or reduce prices to accelerate inventory turnover.

- Better forecasting: Use demand analysis to maintain optimal stock levels

- Creditor Days

- Negotiate longer payment terms: Work with suppliers to extend credit periods.

- Manage cash flow efficiently: Delay payments until the agreed due date without incurring penalties.

- Consolidate purchases: Increase bulk buying to gain favorable credit terms.

- Debtor Days

- Tighten credit policies: Shorten credit terms or require upfront payments.

- Improve collections: Send timely reminders or implement penalties for late payments.

- Screen customers: Assess creditworthiness before extending credit.

- Gearing Ratio

- Reduce debt: Repay loans or consolidate debt with lower interest rates.

- Increase equity: Issue new shares or retain more profits to increase equity.

- Improve profitability: Enhance revenue or cut costs to increase retained earnings.