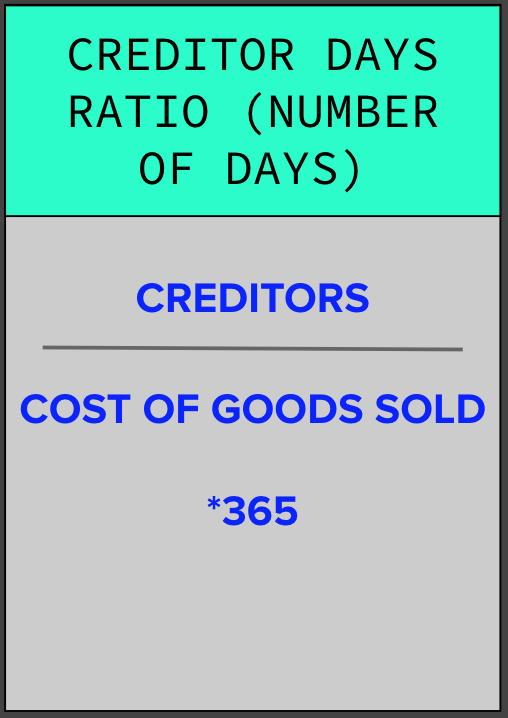

Creditor days ratio measures how many days it takes a business to pay its suppliers. Businesses understand there is a balance between cash flow and paying bills to creditors!

The ratio helps to assesse the credit terms and cash flow management.

Minimum Accepted Value: Too low (paying to quickly) means the company may not be maximizing credit terms, while too high (too slow) can harm supplier relationships!

Better Value: Close to agreed payment terms with suppliers, typically 30–90 days (depending on industry).

Usefulness: Highlights the efficiency of cash flow management and credit utilization.