Unit 3.9 Budgets (HL)

How to allocate cash?

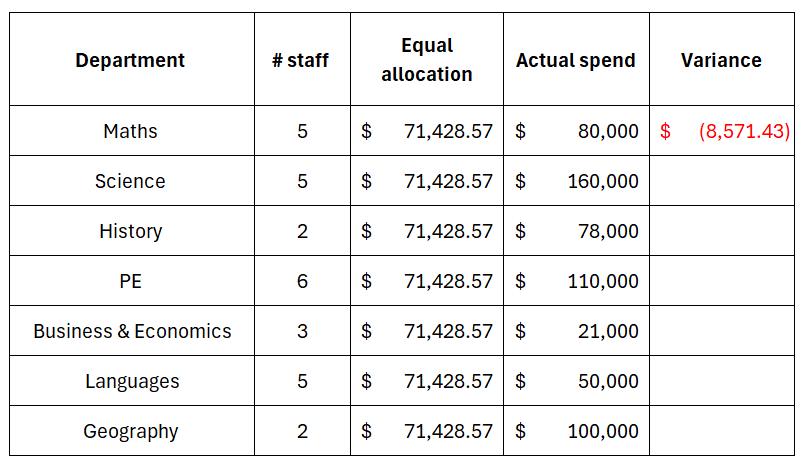

School budget woes

A top international school has been discussing how to allocate money within their functional departments! A range of ideas have been expressed by senior managers. Whilst the school is highly successful, there has been some downturn in student numbers which has prompted the financial manager to start looking at costs and budgets!

To this end, the annual budget has been discussed and a methodology for allocating costs is being discussed! The idea behind this is to share the news with heads of departments, but also allow them to be part of the decision making process and share what they ‘need’ in terms of resources!

Questions

- Define a cost centre

- Looking at the ‘equal allocation’ column, comment on whether you think that each department should receive the same proportion of the annual budget!

- Calculate the variance (the difference between the ‘actual spend’ and ‘equal allocation’.

- Using the calculations from question 2, identify whether or not the variance is adverse or favourable.

- As a manager, which department would you consider to be the biggest cost centre and which the highest revenue or profit centre?

A tense chat

Here’s a dialogue between an unhappy school manager and the head of the IT department regarding an unfavorable budget variance.

- School Manager (SM): Responsible for overseeing the school’s financial and operational performance.

- Head of IT Department (HIT): Advocating for an increased IT budget to address current and future needs.

SM: Thank you for meeting with me today. I noticed that the IT department has already exceeded its allocated budget for this fiscal year by 15%. Can you explain why and what additional funding you’re requesting?

HIT: The overrun primarily comes from an unexpected hardware failure and the need to upgrade several systems that were long overdue for replacement. To maintain the school’s digital infrastructure, we require an additional $30,000 for the remainder of the year. Also, we had a leak which ruined some of our equipment!

SM: I understand the importance, but we must consider the availability of finance! The school’s budget is tight due to recent investments in expanding classrooms, fixing the roof and hiring new staff (due to higher-than-normal turnover). Is it possible to delay some of these expenses?

HIT: Delays could risk operational disruptions, and the parents want to see IT investment. In the past, our department’s budget has been underfunded relative to our actual needs. Benchmarked against schools of similar size and scope, our per-student IT spending is 25% lower, yet we handle increasing technological demands.

SM: Can you demonstrate how additional funding supports the broader educational mission?

HIT: Absolutely. Modernizing our systems directly supports innovative teaching methods, such as interactive lessons and online assessments, which are key to achieving our learning outcomes. Without these upgrades, we risk falling behind competing schools, which could impact enrollment and parent dissatisfaction!

SM: You’ve made valid points. However, the finance committee has flagged the escalating costs in IT as a potential issue. Have you considered alternative ways to manage costs or generate additional revenue?

HIT: We’ve started exploring partnerships with technology companies to secure discounts and sponsorships. Additionally, we could introduce a small tech fee for extracurricular IT services, which might offset some costs

SM: Negotiating partnerships sounds promising, and introducing a tech fee is worth exploring. But for now, I need you to refine your request. What’s the absolute minimum you need to maintain operations without jeopardizing services?

HIT: After reviewing our plans, I can reduce the request to $20,000 by prioritizing only the most critical upgrades.

SM: That’s a start. Here’s the compromise: since IT is a cost center rather than a profit center, we’ll allocate the additional $20,000. However, moving forward, your department must identify sustainable ways to cut costs or bring in additional revenue to avoid similar overruns next year.

HIT: Understood. Thank you for the support. I’ll start looking at who we can fire and also reduce spending on tea bags and milk! We’ll work on implementing the proposed measures to enhance our financial efficiency.

Questions

- Summarise how historical data and benchmarking data were used to discuss budgets in the conversation

- Describe the trade-off between increased spending and reducing a budget in terms of the IT department in a school

- Using the information from the table below, describe how i) planning, ii) coordination, iii) control and iv) motivation and important when considering how to set budgets

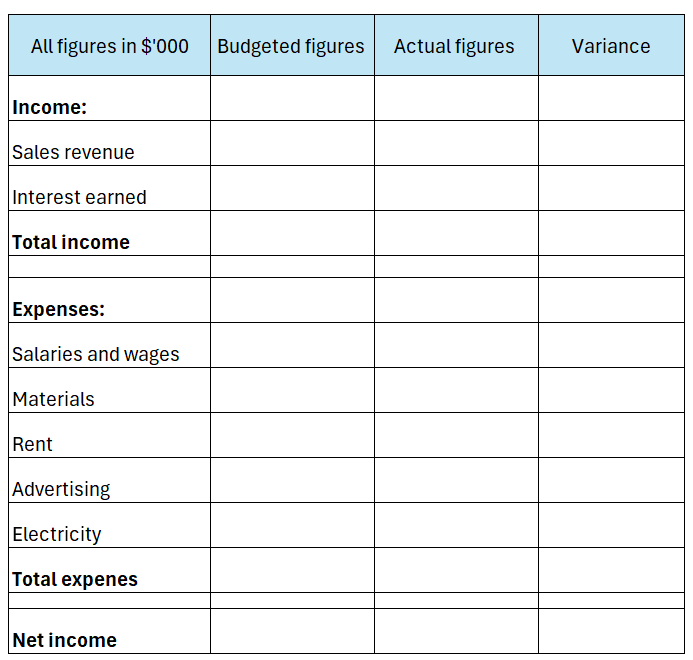

CONSTRUCTING A BUDGET

Memo

To: Finance Department Trainees

From: Chief Financial Officer

Date: January 6, 2025

Subject: Financial Performance Overview

Below are the budgeted and actual financial figures for the past quarter. Please review and calculate the variance for each category, then complete the budget table accordingly.

Income ($’000):

- Sales Revenue: Budgeted: 800, Actual: 750

- Interest Earned: Budgeted: 50, Actual: 60

Expenses ($’000):

- Salaries and Wages: Budgeted: 300, Actual: 320

- Materials: Budgeted: 200, Actual: 180

- Rent: Budgeted: 100, Actual: 110

- Advertising: Budgeted: 50, Actual: 60

- Electricity: Budgeted: 30, Actual: 40

Thank you, and feel free to reach out for clarifications.

Best regards,

[Goward Filmour]

BUDGET CONSTRUCTION TASK

Above are the budgeted and actual financial figures for the past quarter. Please review and calculate the variance for each category, then complete the budget table accordingly.

Instructions:

Use the budgeted and actual figures to calculate the variance (Budgeted – Actual).

Total the income and expenses to determine the Total Income, Total Expenses, and ultimately, the Net Income (Total Income – Total Expenses).

Populate the table with your results, which may look like the example created below!

Additional information on budgets

Cost Centres

Cost centres are parts of an organization that incur costs but do not directly generate revenue. Their focus is on managing and minimizing expenses.

Example: A school’s maintenance department or a business’s IT support team.

Biggest Cost Centre:

School: Facilities and maintenance (e.g., building repairs).

Business: Administration or customer service.

Profit Centres

Profit centres generate revenue and track profitability, contributing directly to the organization’s financial goals.

Example: A school’s cafeteria or a business’s sales department.

Biggest Profit Centre:

School: Extracurricular activities like music lessons or sports programs (if fee-based).

Business: Core product or service sales.

Planning and Guidance

Budgets allow organizations to set financial targets and allocate resources effectively. They provide a framework to anticipate challenges and opportunities, guiding decision-making.

Example: A school might use a budget to plan for an upcoming science fair, ensuring funds are allocated for equipment, prizes, and promotional materials.

Control

Budgets act as a control mechanism by monitoring actual performance against planned objectives, identifying variances that require corrective action.

Example: If a school’s annual events budget exceeds the planned amount due to unexpected costs in a cultural day, adjustments can be made to other areas like school trips.

Coordination

Budgets align different departments or teams by clearly defining financial priorities, ensuring resources are distributed to achieve common goals.

Example: At a school, the sports department and drama club coordinate their fundraising and spending through a shared budget to avoid overlapping resource requests.

Motivation

Budgets can motivate staff by involving them in the budgeting process and setting achievable financial goals tied to performance incentives.

Example: A school principal might motivate teachers by allocating a portion of the budget for classroom innovations, encouraging creative teaching methods.